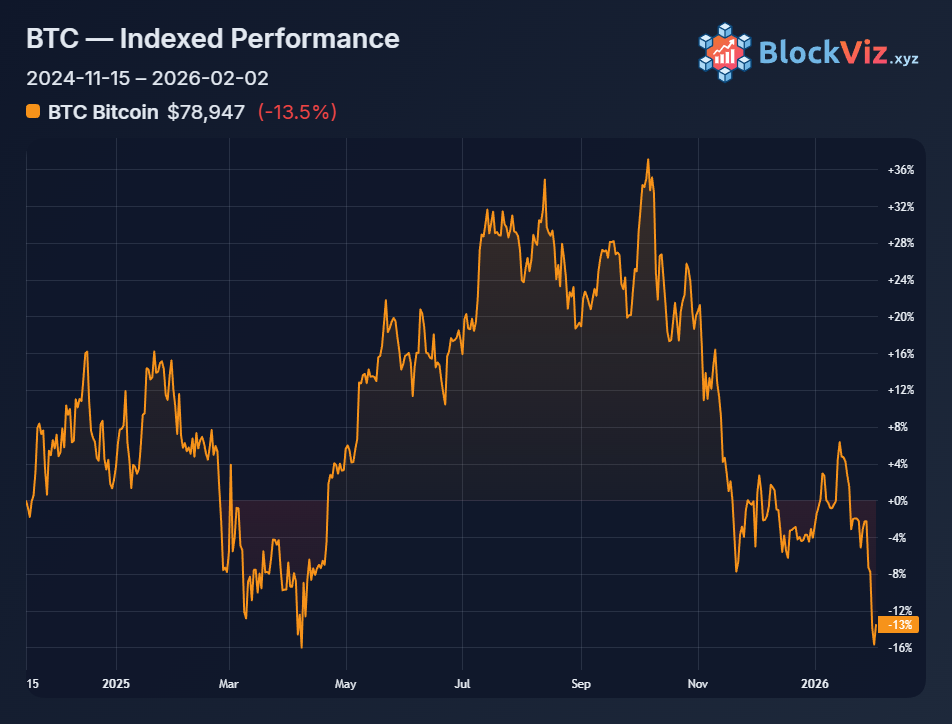

MicroStrategy's Bitcoin stack just flashed red. With $BTC dipping below their average buy price today, their massive position shows paper losses of around the high nine figures.

The company holds over 700k BTC at an average cost near the mid 70k region, putting total fiat invested north of 50 billion dollars. As BTC traded briefly below that level on February 2, the treasury slipped underwater by low single digit percentages before recovering slightly with the intraday bounce.

The reason it hurts now is simple. BTC just sold off sharply from fresh all time highs, wiping a big chunk of market cap in a few sessions as macro jitters and profit taking kicked in. MicroStrategy’s equity trades like a high beta BTC proxy, and the market is suddenly re‑pricing the risk of a debt‑levered Bitcoin balance sheet.

The warning case is about structure, not conviction. MicroStrategy financed a lot of its stack with convertible debt and ATM equity issuance. If BTC stays below their cost basis for long, renewed selloffs in the stock could force more dilution or make future raises tougher and more expensive, especially if credit conditions tighten.

The opportunity case is about time horizon. This is not the first time their position has gone deep red on paper; prior drawdowns in 2021–2022 eventually flipped back into profit as the cycle matured. For long‑term BTC bulls, a moment when the most aggressive corporate buyer is temporarily underwater has historically lined up closer to accumulation zones than blow‑off tops.

For the CoinMarketCap crowd the key questions are clear. Does the market start to price in solvency and funding risk around MicroStrategy’s structure, or does it again reward long term BTC beta once the next leg higher starts? Watching how BTC trades around their average cost level will tell you whether this is just another buyable shakeout or the first real stress test of the “Bitcoin as a public company balance sheet strategy” narrative.