Interpretation

What problem this visualization solves

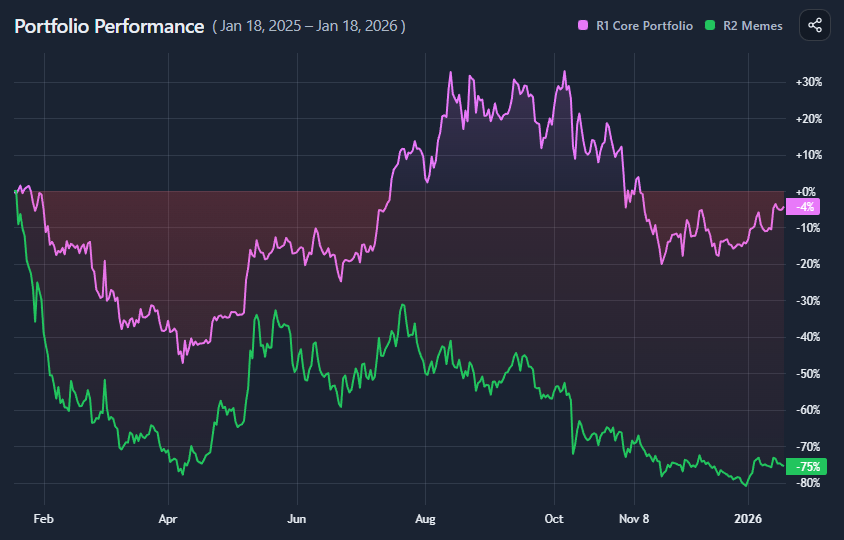

Comparing portfolios by absolute value is misleading.

A portfolio that starts with more capital will almost always look “better” in raw dollar terms, even if its allocation decisions were worse. Similarly, comparing a real portfolio against a model allocation is difficult when their starting values differ.

Portfolio Comparison removes this distortion by normalizing every portfolio to the same starting point.

What you’re looking at

You are looking at an indexed performance chart for portfolios.

Each portfolio is rebased to 100 at the selected start date. From that point on, the chart shows relative returns, not absolute value.